Should You Lease or Buy a New Vehicle?

A Holistic Approach to Prosperity

February 2015 Interview with Laurie Bonser; Natural Awakenings Magazine by Sandra Yeyati

February 2015 Interview On Holistic Financial Planning

Ways to Avoid a Financial Catastrophe

Starting a New Business

With the new year right around the corner, many people are thinking about starting their own new business – whether as a full time venture or part time opportunity. Here are some important questions to ask yourself as part of considering this big step:

- How do I make a good transition between my current job and income into my new endeavor?

- How do I make the best use of my own resources and finding others to help my business?

- What can I do to minimize the risks of starting or expanding my business?

- How do I balance my personal and business finances for the best overall outcome?

- What information do I need to manage and measure the success of my new venture?

- How can I make really conscious, thoughtful decisions right from the beginning to focus my efforts and align choices with my overall goals?

Best wishes for much enjoyment and satisfaction in your new endeavor!

Author Pens Best Selling Financial Book

Ballston Spa Author Pens Best -Selling Selling Financial Book

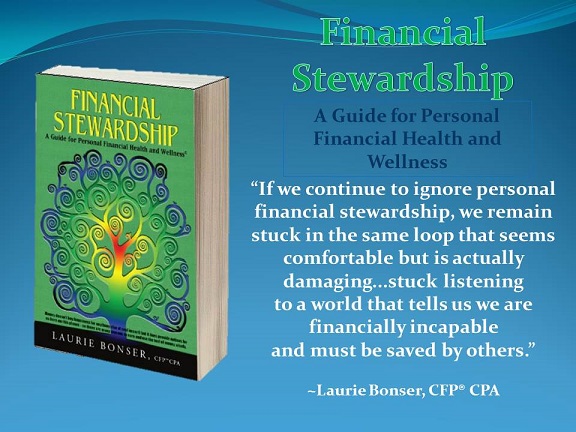

SEPTEMBER 21, 2014 BY STEPHANIE HALE-LOPEZ BALLSTON JOURNAL, BALLSTON SPA,NY – Laurie Bonser, CFP, CPA, and owner of Changing Times Planning , recently hosted a book launch for her newly released book, Financial Stewardship: A Guide for Personal Financial Health and Wellness. Dozens of community members attended the launch event at Lake Ridge Restaurant Wednesday and picked up copies of Bonser’s book, which has already been named to Amazon’s bestsellers list.

Laurie Bonser, author of Financial Stewardship: A Guide for Personal Financial Health and Wellness, at her book launch Wednesday, Sept. 17. Bonser has an eclectic background. Aside from being a CPA, Certified Financial Planner professional and coach, Bonser is also a musician, teacher, reader, and shaman who explores Reiki, MAP, plant spirit medicine, animal communication, and other healing resources. “[The book] really tied together everything from my music background, the work and the study that I had to do to become a CPA and CFP, and my interest in animals,” said Bonser. “I have friends in all sorts of different professions so it was really meant to be not only a book on financial planning, but a real holistic look at life and how we made decisions and choices.” Financial Stewardship isn’t your typical book about finances. The unique guide shows readers how to shift perceptions of personal finances from a numbers-oriented view to a rewarding one, encompassing individual needs, goals and ownership to benefit health and wellness. “I was motivated this winter with all of the snow and ice and everything, to sit down and write this,” said Bonser. “I guess it had been rolling around in my head for quite some time. I started writing in the middle of January and in the middle of April, it just kind of came all pouring out.”

Bonser says her book is meant to serve as a guide to financial fitness and that more people need to take into account their financial health and wellness. “You make changes to your diet slowly over time, or you come to an awareness that some foods don’t sit well with you, so that was in the back of my mind with the book,” said Bonser. “You don’t have to be a math whiz to know everything about the stock markets or investments. Financial planning is very much like going to your general physician and practitioner over time, because you go for periodic check-ups. I tried to use some of those analogies, because they made sense to me.”

Financial Stewardship: A Guide for Personal Financial Health and Wellness is an Amazon best-seller. The main message Bonser says she wanted to get across in her book is that money is just a tool. She says she wants to give people the knowledge and confidence to manage their own financial stewardship goals in actual planning, conversations and decisions. While everyone’s financial situation is different, Bonser does have some advice people can start implementing immediately to better their financial position. “Give yourself permission and the time to sit down and think about making your decisions,” said Bonser. “Don’t feel pressured or that it’s a deal of the day that you have to take advantage of. One of the other big things is to communicate and to get more comfortable talking with our partners and our spouses. If we’re not communicating with each other, we’re just making assumptions. Think about talking about money and finances as part of building relationships while taking your core values into consideration.”

Financial Stewardship: A Guide for Personal Financial Health and Wellness is currently available at Northshire Bookstores in Saratoga Springs and Vermont, as well as Amazon and Barnes & Noble . “Somebody told me this winter is going to similar to last year’s winter with the weather,” said Bonser. “So I may have to bundle up and write some more.” Laurie Bonser lives in Ballston Spa and may be reached through her website .

The new ‘Financial Stewardship” book is now available!

I feel rather like Tigger bouncing around this week with the actual publication of my new book ‘Financial Stewardship: A Guide for Personal Financial Health and Wellness”! After many months of writing, designing, editing, and finding the right path in the publishing realm, the messages are now ‘official’ and available in paperback and eBook formats through Northshire Bookstore, Amazon, Barnes and Noble and many other avenues (Please see the links on the Book tab on the menu bar). I look forward to all the future discussions, additional ideas, and transformations that will come from this collaborative effort. Thank you for being part of this momentum.

Companion Animals: Planning for Ourselves and Our Pets

One of the standard questions I ask new clients is whether they have companion animals. While pets are such an integral part of our daily lives, it’s not uncommon to overlook making special arrangements for their care in the event that we ourselves become ill or pass. There are a number of simple, straightforward options available for all of us to gain peace of mind in this area, both for ourselves and our furry companions, including pet trusts, setting up savings or life insurance plans, planning with local animal foundations, making provisions in our wills for care and guardianship, and more. Be sure to ask your planner or estate attorney for some specific guidance in your particular situation. And please also consider either using or supporting the Pet Peace of Mind program with a local hospice organization if you or someone you know needs assistance keeping that wonderful bond between human and companion together.

Pet Peace of Mind Video:

Common Misconceptions about Long Term Care

I could talk for quite a while about why planning ahead for our health care is so very important for ourselves and our loved ones…and why setting up savings and possibly insurance solutions are key to maintaining our choices, independence, and dignity. But for today’s post, I’ll focus on sharing five top misconceptions about long term care to offer some food for thought for the week.

1) Long term care issues are for older seniors only. Actually, over one-half of those people needing long term care attention are under the age of 50 – due to unexpected illness, accidents, and early onset of diseases. We pay for home and auto insurance, for example, and hope we don’t need to go through the experience of using it – but yet health issues may also sideline us at any time too…and it’s a prudent part of planning to protect that very valuable asset too.

2) Long term care equates to nursing home care. Most people who need long term care will benefit most from home care and assisted living – and that’s where most people would prefer to stay to enhance their comfort and quality of life. It’s definitely not a choice between no care and a skilled nursing home/hospital setting.

3) You should wait until your 60’s before looking at long term care planning. You may need long term care at any age (see point #1) and if you are thinking about using long term care insurance as some form of risk sharing, then waiting until age 60 and over could well be too late – as insurance gets progressively more expensive later in life and there’s also a much higher chance that you will have developed some health problem(s) before then that could adversely affect policy underwriting. So it may well make sense both financially and personally to be insured at a much younger age.

4) Long term care insurance is too expensive so I’m not even going to look at it. It’s true that many of the original insurance policy premiums written 10-20 years ago have increased quite a bit due to the current low interest rates, low lapse trends, and top end features. However, there are plenty of newer solutions available to provide flexible coverage – often with state tax benefits, pooled benefits for couples, and custom riders – so it’s a smart move to meet with an experienced professional to get the real scoop.

5) Medicare will cover long term care if I need it. All publicly funded programs are under immense financial pressures and this situation will only increase in coming years with a larger population. So, first, any current benefits such as for home hospice care and skilled nursing will likely be further constrained going forward. Secondly, under such general programs, there is very limited personal choice and flexibility for care options – rather a “take it or leave it” last resort scenario as these types of programs were originally intended as a final safety net only. And even when people do meet the health care criteria for coverage, income and assets must be greatly reduced before Medicare begins payment.

Financial Stewardship Choices

Excerpted from my new book Financial Stewardship: A Guide to Personal Financial Health and Wellness©, July 2014

Choices

‘Making conscious choices in our lives is the basis of honoring our intentions and callings. And the area of financial stewardship is an integral part of that process. It’s just as important to consider these decisions and choices as it is to review your physical health or relationships because finances influence many of our thoughts and communications, whether consciously or otherwise. Having a healthy dialogue about money choices can reflect positively on our personal relationships, our work alternatives, meeting future goals, our personal power and impact, how we can help change future community conversations about financial issues, and much more.

Consider:

How do I give choices about financial matters a lower priority in my life – and why and when?

What other areas of my life are affected by my choices (or lack thereof) regarding money?

What benefits could I have by taking a more active role in the financial stewardship of my life?’